The $10,000 threshold for Currency Transaction Reports is one of the most widely known numbers in financial compliance. It is also one of the most deliberately exploited. The moment a regulatory trigger becomes public knowledge, a segment of bad actors begins designing around it. With CTRs, that design looks like structuring.

Structuring is the practice of deliberately breaking up cash transactions to stay below the CTR reporting threshold. It is not a fringe financial crime tactic. It is one of the most commonly prosecuted Bank Secrecy Act violations in the United States, and it shows up across nearly every sector that handles significant cash volumes. Understanding how it works, and how compliance programs reliably detect it, is essential for any financial institution managing cash transaction reporting obligations.

What Is Structuring Under the Bank Secrecy Act?

Structuring is defined under 31 U.S.C. § 5324 as breaking up or arranging cash transactions specifically to evade the CTR filing requirement. The law is deliberately broad. A person does not need to be involved in another underlying crime to be charged with structuring. The act of intentionally keeping transactions below $10,000 to avoid a report is itself the federal offense, regardless of whether the cash itself came from illegal activity.

That distinction catches many people off guard. Structuring does not require proof of money laundering, drug trafficking, or any predicate crime. Federal prosecutors have successfully charged individuals for structuring proceeds from otherwise lawful businesses, simply because those individuals knew about the reporting threshold and deliberately stayed beneath it.

The maximum criminal penalty for structuring is five years in federal prison, rising to ten years when the conduct is connected to other criminal violations. Civil forfeiture of the funds involved is also common, meaning the government can seize the structured cash even when criminal charges are not pursued.

How Structuring Actually Happens in Practice

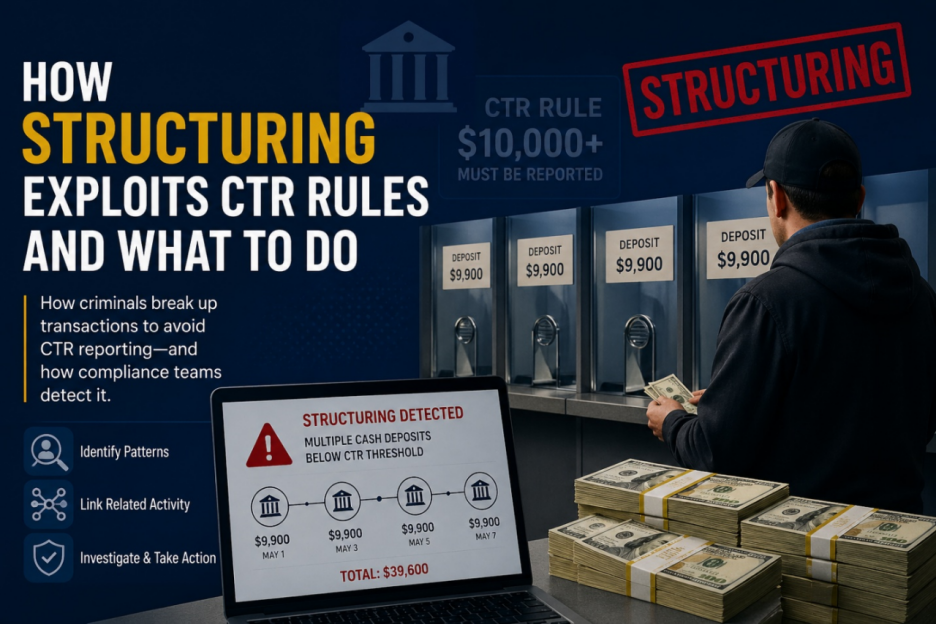

The mechanics are straightforward. Instead of depositing $15,000 in a single transaction, a person makes three separate $5,000 deposits across different days, different branches, or even different banks. The individual transactions never cross the reporting threshold. Without aggregation and pattern recognition, each one looks unremarkable.

Smurfing: The Distributed Version

When structuring involves multiple people acting on behalf of one, it is called smurfing. A single principal will recruit or pay individuals, sometimes called “smurfs,” to conduct cash deposits or purchases at various institutions. Each smurf handles a series of small transactions that fall below the CTR trigger, while the aggregate funds move toward a central destination.

Smurfing is more complex to detect because the transactions are dispersed across different accounts, different institutions, and sometimes different geographic areas. The connection between the smurfs and the principal may not be obvious from transaction records alone.

Structuring Through Purchases and Withdrawals

Structuring is not limited to deposits. It also appears in cash withdrawals, purchases of monetary instruments like money orders or cashier’s checks, and in some cases wire transfer initiation. Any situation where the BSA reporting threshold is deliberately avoided can qualify as structuring, regardless of the transaction direction.

Casinos, car dealerships, jewelry stores, and currency exchange businesses have all been enforcement targets because their cash-intensive operations create natural cover for structured transactions. Financial institutions that serve these industries carry elevated structuring risk and face heightened regulatory scrutiny as a result.

Why the $10,000 Threshold Is a Blunt Instrument

The CTR threshold has remained at $10,000 since the Bank Secrecy Act established it in 1970. Adjusted for inflation, that figure would be well above $80,000 in today’s dollars. The static threshold means that a much broader range of ordinary transactions technically approaches or crosses the reporting line than was ever originally intended, which creates two compliance problems simultaneously.

First, it generates a very high volume of CTR filings, the vast majority of which have no connection to financial crime. FinCEN receives millions of CTRs annually. That volume strains law enforcement’s ability to analyze the data meaningfully, particularly when the signal-to-noise ratio is poor.

Second, and more relevant to compliance teams, the widely known threshold makes the structuring detection challenge much easier for criminals than it should be. There is no mystery about what to avoid. The sophistication required to structure transactions is minimal, which is part of why it remains so prevalent despite decades of enforcement activity.

A thorough understanding of how CTR filing requirements fit within the broader AML reporting framework helps compliance teams appreciate why structuring detection cannot rely on threshold monitoring alone. CTRs catch what crosses the line. Detecting structuring requires identifying patterns in what stays below it.

What Does Reliable Structuring Detection Look Like?

Catching structuring requires aggregating transaction data in ways that individual tellers, relationship managers, or manual review processes simply cannot do consistently at scale. The following approaches form the foundation of any serious structuring detection capability.

Aggregation Across Time and Accounts

The most basic structuring detection rule aggregates a customer’s cash transactions over a rolling window, typically 10 to 30 days, and flags when the combined total approaches or exceeds the CTR threshold across multiple transactions. A customer who deposits $4,900, $4,800, and $4,700 over the course of two weeks has not triggered a single CTR. But the aggregate pattern is textbook structuring.

More sophisticated programs extend aggregation across accounts, not just individual customers. A business owner who splits cash deposits across a personal account and a business account, or a smurfing network where funds are dispersed across multiple individuals, requires relationship mapping to detect. Transaction monitoring systems that operate at the account level without linking related parties will miss these patterns consistently.

This is where fragmented, legacy compliance tooling consistently falls short. When transaction monitoring, customer risk data, and relationship mapping live in separate systems, the aggregation logic required to surface structuring patterns simply cannot operate as intended. Compliance teams end up manually bridging data gaps that an integrated platform would close automatically, which creates both detection delays and documentation inconsistencies that regulators notice during exams.

Velocity and Frequency Analysis

Structuring often produces distinctive velocity signatures. A customer who rarely made deposits suddenly begins making multiple small cash deposits per week, or one who previously made single large deposits begins fragmenting them across multiple branches. The change in transaction behavior is itself a signal, independent of any single transaction amount.

Velocity rules that establish behavioral baselines for each customer and flag significant deviations are more sensitive to structuring patterns than static threshold rules. They are also less prone to generating false positives from legitimate high-volume cash businesses, because the baseline accounts for that customer’s normal behavior.

This is precisely where AI-native financial crime compliance platforms create a meaningful operational advantage. Rather than relying on fixed rules that treat every customer identically, AI-driven systems build individualized behavioral models that adapt as customer activity evolves. That dynamic baseline approach detects structuring attempts that static rule sets would miss, while simultaneously reducing the false positive volume that burdens compliance teams in legacy environments. Critically, the AI’s recommendations remain transparent and auditable, so compliance officers can follow the reasoning behind each flag, validate it against the underlying data, and document their decision with confidence. That explainability is not incidental. It is what makes AI-assisted detection defensible under regulatory scrutiny.

Geographic and Channel Dispersion

Structured transactions often appear at multiple branches, ATMs, or correspondent institutions rather than a single location. Geographic dispersion rules flag customers who conduct cash transactions at an unusual number of locations over a short period. A customer who makes deposits at five different branch locations in a single day, with each transaction under $3,000, is exhibiting a pattern that warrants review regardless of the individual amounts.

Monetary Instrument Purchases

Structuring frequently involves purchasing money orders, cashier’s checks, or prepaid cards with cash in amounts just under reporting thresholds. Financial institutions are required to file Currency Transaction Reports for monetary instrument purchases over $3,000, and to keep records for purchases between $3,000 and $10,000. Compliance programs that monitor monetary instrument purchases separately from deposit transactions catch a dimension of structuring that deposit-only monitoring misses.

The Suspicious Activity Report Connection

Detected structuring does not automatically produce a CTR. By definition, structured transactions individually fall below the reporting threshold. What they do produce is a Suspicious Activity Report obligation. Under FinCEN guidance, financial institutions that identify structuring patterns must file a SAR documenting the suspicious activity, the transactions involved, and the basis for the determination.

The SAR filing requirement for structuring is one of the most litigated areas of BSA compliance because it requires subjective judgment about intent. Structuring requires evidence that the transaction fragmentation was deliberate. An elderly customer who simply prefers to make small frequent deposits out of habit is not structuring. A business owner who switches from weekly bulk deposits to daily sub-threshold deposits immediately after a conversation with a teller about CTR requirements is a much stronger candidate for a SAR.

This is where AI forensics capabilities add measurable value to the investigation workflow. When a structuring pattern surfaces, specialized AI agents can rapidly pull together the full behavioral context behind the flagged transactions, cross-reference prior account activity, map relationships to linked accounts, and generate a structured investigation summary that compliance officers can review, validate, and use as the documented basis for a SAR filing decision. The AI handles the time-consuming evidence assembly. The compliance officer retains full control over the final judgment, with every step preserved in an auditable trail that regulators can follow. That division of labor, where AI accelerates investigation without displacing human accountability, is the standard that serious financial institutions should hold their compliance technology to.

Compliance teams need documented decision frameworks for evaluating potential structuring cases, including clear standards for what constitutes sufficient evidence of intent to warrant a SAR filing. Programs that operate on institutional intuition rather than documented criteria create both exam risk and litigation exposure.

High-Risk Sectors and Customer Profiles

Structuring risk is not evenly distributed across a financial institution’s customer base. Certain industries and customer profiles carry significantly elevated exposure and warrant enhanced monitoring.

Cash-intensive retail businesses including restaurants, convenience stores, parking operations, and laundromats provide natural cover for structured deposits because their daily revenue patterns involve frequent small cash transactions. Distinguishing legitimate operational deposits from structured ones requires understanding each business’s normal transaction behavior.

Real estate transactions have long been a concern for structuring and layering activity, particularly in markets with significant cash sales. Financial institutions involved in real estate-related accounts should monitor for cash activity that precedes or follows property purchases or refinancings.

Peer-to-peer payment platforms and money service businesses face elevated structuring risk because their transaction models involve high volumes of smaller payments that can mask aggregate cash movement. The intersection of digital payment infrastructure with cash on-ramps and off-ramps is a priority monitoring area for FinCEN.

Foreign national accounts and accounts with significant international transaction activity are also higher risk, particularly when cash deposits appear alongside frequent international wire transfers. The combination of structured cash deposits and cross-border movement is a classic money laundering typology.

For institutions managing high-risk portfolios across multiple sectors, the ability to configure detection logic by customer segment and risk tier is not optional. A compliance program that applies the same monitoring parameters to a cash-intensive convenience store chain and a low-volume retail investor account will generate either chronic over-alerting or significant blind spots. Flexible, customizable rule infrastructure, backed by a delivery team that understands how complex institutions actually operate, is what allows detection programs to scale accurately rather than just noisily.

What Enforcement Looks Like When Structuring Goes Undetected

Regulators do not just penalize institutions for failing to detect structuring. They hold institutions accountable for failing to maintain adequate detection capabilities. The distinction matters because it means that ignorance of a structuring pattern is not a complete defense when the monitoring program was inadequate to detect it.

FinCEN and banking regulators have issued significant penalties against financial institutions whose transaction monitoring systems lacked the aggregation logic needed to identify structuring patterns. In several enforcement actions, regulators cited the absence of multi-account aggregation, the failure to monitor for monetary instrument structuring separately from deposits, and the lack of any velocity-based behavioral analysis as program deficiencies that contributed to undetected BSA violations.

Flagright is built specifically to address these program gaps at an enterprise level. Trusted by more than 100 financial institutions across 30-plus countries, the platform functions as an operating system for financial crime compliance, unifying transaction monitoring, watchlist screening, case management, and governance controls in a single audit-ready environment. Its detection capabilities cover multi-account aggregation, behavioral velocity analysis, geographic dispersion monitoring, and monetary instrument tracking. AI capabilities are embedded throughout, supporting alert investigation, system optimization, and risk-based recommendations in ways that are transparent, explainable, and designed to keep human oversight intact. For institutions moving beyond rigid or fragmented legacy infrastructure, it provides the auditability, control, and long-term operating confidence that sophisticated financial institutions require.

Building a structuring detection program that satisfies regulatory expectations requires more than a single rule. It requires layered controls that cover aggregation, velocity, geographic dispersion, and monetary instrument purchases, with documented review processes for every flagged case and clear SAR filing criteria that compliance officers can apply consistently.

The institutions that have weathered BSA enforcement scrutiny most successfully are those that built detection infrastructure before an examination revealed the gaps, not after.